Business Protection - Control and Certainty

Super Advice NZ provides specialist life risk facilitation and advice services to business owners and executives. We have a focus on providing services in relation to business succession, key person, loan guarantor and personal protection needs. Our objective is to protect your business and the owners against the impact created by an unexpected death, disability or critical illness of key people or equity partners.

When advising clients in relation to their business protection and succession planning needs, there are three key principles which are carefully considered:

Asset Protection

If business debts are secured by personal assets, have the consequences of personal guarantees been considered?

Revenue Protection

Would the loss of a key employee result in a loss in revenue and profitability?

Ownership Protection

Would the loss of an owner result in a loss in business value or worse still, control of the business?

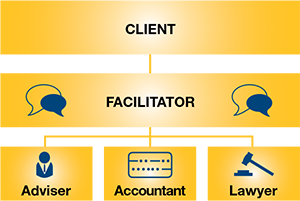

How does the facilitation process work?

As facilitators, we will work closely with your team of advisers (accountants, lawyers, etc) to project manage a business protection and succession plan specifically tailored to your business.

Our unique process allows us to coordinate funding and legal solutions in a timely and cost effective way, that ensures you can focus on what you do best; running your business.

Revenue Protection

Cash flow is KING

Key person protection allows a business at a time of great uncertainty, to reinvest in itself providing stability and certainty if a key person suffers a premature death, is diagnosed with a critical illness or is disabled.

Are you a key person?

A key person is someone who provides the ideas, drive, initiative and skills that propel a business forward.

Key people can include:

- Business Founders and Principals

- Managing Directors

- Key Sales staff

- Key Investors

How do you benefit?

The aim of this cover is ultimately, to protect revenue and profitability.

The protection can be used to:

- Provide funding to repay outstanding debts, thus protecting your credit rating

- Provide lump sum income to offset additional and unexpected costs

- Stabilise the business financially

- Provide additional funding to meet recruitment, retraining and familiarisation expenses

Asset Protection

Loan guarantor protection ensures that personal assets that are subject to personal or directors guarantees, are protected upon death, illness or permanent disability of a business owner who guarantees a loan.

How it works

Often an owner will secure a loan with their personal assets (e.g. the family home). Only when the loan is repaid in full, will the guarantee be extinguished. Loan Guarantor Protection insurance is used to pay out these loans if the business owner dies or becomes incapacitated. Most importantly it protects the guarantors personal assets and ensures control is retained.

Ownership Protection

Many New Zealand business owners generate and lock up their wealth in their business. Therefore it makes sense to protect this, yet many fail to do so.

How do you benefit?

A Business Succession Plan ensures equity positions (and its value) within a business are protected if an owner is forced from the business due to critical illness, death or disability.

A properly constructed plan will not only provide certainty, but the following outcomes too:

- A ready market for the business interests

- Ensures equity remains tightly held by the right people

- Allows for an orderly, commercial transition of ownership

- Provides a funding mechanism for the remaining owners

- Ensures control of the business remains with the right people

There are two components to a properly constructed business succession plan and without either one present, the plan is likely to fail.

The first component is a correctly drafted and executed business succession agreement. This is a formal document signed by all parties outlining exactly what happens in the event a trigger event occurs. The agreement ensures certainty, by creating ready buyers, and sellers, for the equity at a fair and pre-determined price and ensures a terminating owner receives true value for their stake.

The second component is a funding mechanism which allows capital to become available at any point in time, to fund any buy out of equity. It's possible that this capital can come from several sources, however the most efficient source by far is to outsource the funding to a third party. In this case through an insurance policy that responds by paying the right amount of capital at the right time.

Business Expense Protection

In the event that you become totally or partially disabled due to an injury or sickness, business expense protection provides you with a monthly benefit to meet the fixed costs and overheads of running your business.

An example of some of the costs (but not limited to) covered by the plan are as follows :

- Salaries of administrative employees

- Office rent / lease payments

- Regular business mortgage repayments or business loan instalments

- Equipment leasing costs

- Electricity, gas, water and telephone costs and other utility costs

- Accountant fees

The policy works in tandem with a personal income protection policy; it ensures that any fixed business expenses are not funded by your income needed to pay for your personal living expenses. A Business Expenses policy will fund up to 100% of the fixed business overheads for a period of up to 1 yr. Being able to meet these fixed costs while revenue is not being created will ensure that your business stays operational while you are recovering from your injury or sickness.